Here is one thing I think I am thinking about three times.

1) The money supply as the cost of capital.

In a recent interview MicroStrategy CEO Michael Saylor was criticizing Warren Buffett’s cash management. Buffett has a colossal cash hoard of $325B sitting in T-Bills earning 4.5%. Saylor, on the other hand, invests his cash in Bitcoin. He justifies this “cash management” by arguing that his “cost of capital” is 15%. Saylor makes this claim by arguing that the money supply is increasing by 15% and that that is essentially the real cost of future money.

Oh boy. Where do we even start with that? I hesitate to criticize Saylor because this bet has worked out brilliantly so far, but that doesn’t change the way economics and finance works.

First, I have to defend Buffett for obvious reasons. Warren Buffett is the greater capital allocator in human history. The essence of Berkshire Hathaway is that it’s a cash flow monster that he has masterfully allocated across time. Cash management isn’t just something he’s good at. It’s why he is who he is. And a crucial element of that is in understanding that he allocates his cash in productive entities while leaving roughly 10% of his capital in a liquid form to be deployed when needed. There’s absolutely nothing wrong with buying Bitcoin and it’s worked out beautifully so far for MSTR, but Bitcoin is not cash. In fact, Bitcoin increasingly looks like a levered form of QQQ. And the whole point of owning something like TBills is that they can be deployed when things like QQQ become discounted. If BTC were to crater for some reason MSTR would not be able to lean into this “cash” holding and in fact, there’s a very real chance that the internal leverage could result in them becoming forced sellers of BTC. It’s not just dissimilar to what Buffett is doing with TBills. It’s almost the opposite of the way Buffett thinks about dry powder. And in fact, Saylor is funding his BTC purchases…wait for it, by selling bonds to obtain fiat. The difference between him and Buffett is that he isn’t using organic cash flows to fund the asset purchases and is instead getting his fiat from lenders.

Second, the money supply isn’t inflation. That’s like saying that calories are fat. Sure, if you eat too many calories and don’t put your calories to good use by being active then you will get fat. Similarly, if we just printed off money and didn’t do anything productive with it then that money would just lead to inflation. But that’s not what actually happens. Money creation very often (not always) leads to productive uses that create real resources and are therefore deflationary in many cases or inflation neutral. That’s why economists specifically measure inflation based on the change in prices of a basket of consumer goods. You can’t just say “NVIDIA borrowed $100M from JP Morgan therefore inflation will go up”. No, NVIDIA is very likely creating money and then using it in a manner that will be accretive to earnings and generate real resources that are inflation neutral in the long-run. Of course, it’s also true that government spending is often inflationary. We experienced very high inflation during Covid in large part due to government spending. But even then the 15% assumption is wildly overstated.

Don’t get me wrong. There are lots of smart reasons to own something like Bitcoin and I am not some anti-coiner type. But sometimes the narratives are a bit much.

2) TradFi’s inability to adopt Bitcoin

I guess I am what Bitcoin Maximalists might call a “traditional finance” (tradfi) guy. I’ve long stated that there are perfectly rational reasons to own Bitcoin. I believe this is especially true if you live in a 3rd world economy where the probability of currency collapse is even moderately high. I believe the story is more complex for US investors where the Dollar is so stable. When it comes to practical money management it’s an asset you might want, but don’t necessarily need. I think most people in tradfi think of Bitcoin somewhat similarly.

I’ve mentioned this in the past, but Bitcoin falls into the Defined Duration model as a form of insurance. It’s a super long duration instrument that exhibits huge asymmetric upside at times and gives you an insurance hedge against fiat currency. The question someone has to ask themselves about an asset like this is:

a) Do I need insurance of this type?

b) If yes, then how much?

These are super personal questions and in the case of a US investor I’d argue the use case isn’t nearly as compelling as the use case for someone in, say, Argentina. When you think of it as a form of insurance there’s nothing within traditional finance that says this is wrong. In fact, traditional finance mastered the art of selling insurance to people. But there’s nothing wrong with a traditional finance portfolio holding something like Bitcoin. I just think you have to compartmentalize it properly and thinking of it as insurance has helped me understand the use cases without getting caught up in all the competing narratives about it (or worse, dismissing it entirely).

3) The worlds best (or worst) investment bank.

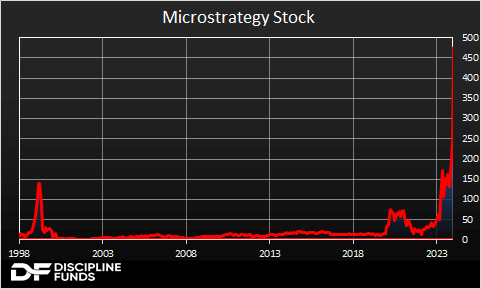

Speaking of Microstrategy – I can’t stop loving this story. I’ve said this for year now, but it’s either the greatest thing to ever happen in finance or it’s the most reckless thing to ever happen in finance. I have no idea which, but there’s really no inbetween in my view. To some degree it’s all very ponzi-like. MSTR is selling bonds to fund purchases of BTC and those purchases help drive the price of BTC up which allows MSTR to finance more bonds. It’s magnificently brilliant as long as the price of BTC keeps going up. As long as it keeps going up.

I’ve joked that MSTR has turned into the world’s most successful investment bank except instead of helping finance capital formation they’re just financing number go up. And look, it’s worked brilliantly so far. Saylor is winning. In fact, you could argue he’s won. He could walk away right now and say “I won all of finance forever and ever”. MSTR is up 3,000% in the last 5 years. Which kinda makes you wonder – if Saylor is right that the cost of capital is 15% per year then MSTR has generated about 24 years worth of returns in just the last 5 years. When do you step back and say “I won”? Or do you? Can you?

I don’t know the right answer. I’m just a boring old traditional finance guy. But me personally – I’d be real tempted to pack up my bags, declare victory and go buy…anything I wanted.