Here are some things I think I am thinking about.

1) Is Inflation Dead?

One of the main themes here this year was that the rate of inflation would gradually decline all year. And while that’s been right the rate of inflation hasn’t slowed enough for the Fed’s comfort level. But this was an interesting week for the inflation outlook because the narrative is now taking a turn in the deflationary direction.

Home Depot and Walmart both reported earnings and said that the worst of the inflation is behind us. Walmart actually said that they think they’ll see some deflation in the coming months. These comments are especially interesting in the context of the CPI report that came out this week, which showed lower than expected inflation despite a 6.7% year over year reading in shelter. That’s important because if you strip out housing the CPI would be just 1.5%. ONE POINT FIVE PERCENT.

So, this is no longer just me projecting now. Not only do we know that shelter is making inflation look irrationally high, but we also know that the most important retailers in the US economy are saying exactly what the CPI ex-shelter says.

Inflation isn’t dead. But it is becoming increasingly clear that inflation is much lower than the Fed’s rate positioning would make us think.

2) The Worst Narrative in Finance.

There was a huge chart in the lobby of my old Merrill Lynch office that showed the average returns of stocks and bonds. Every client who sat in the office would be forced to stare at this massive chart. It showed the average long term returns of stocks at 10-12%. I’ve previously stated that the worst narrative in finance is the way we communicate time horizons to investors. But I don’t think that’s right. The worst narrative in finance is this idea that stocks generate 10%+.

The reality is that stocks have averaged about 4.4% according to Dimson (2020) or 6.6% according to Siegel (2014). A lot of this depends on which market you look at and what time horizon, but the global stock market has generated nowhere near 10% when you account for real factors like inflation, taxes and fees. And that’s important because we don’t live in a nominal world. We live in the real world where we pay for inflation, taxes and fees over time.

I hate to sound like a skeptic about this, but my guess is that the reason many investment firms promote the 10%+ figure is because they are either ignorant of these facts or, more likely, they want to frame returns as being high because their fees are high. After all, if you charge 1% fees then 1% of 10% doesn’t sound so bad. But if you charge 1% on a 5% return then that suddenly sounds like a pretty high fee.

This came to the fore this week because Dave Ramsey was on his show promoting an 8% withdrawal rate based on a 12% average annual return.1 He said that a real return of 8% means that rules like the 4% rule are silly. I can’t tell you how dangerous this is. When you shift towards retirement your time horizon and risk profile shifts to a more conservative position. You can’t be fully invested in stocks when you’re nearing retirement because that creates enormous sequence of return risk. In other words, if you’re 65 in 2007 and 100% invested in stocks and then 2008 happens then you end up going back to work until you’re at least 70. That’s a lifestyle DISASTER. And the only way that disaster happens is if your financial planner is making irrational projections about asset returns and your asset allocation.

Anyhow, I don’t mean to beat up on Dave, but the reason why rules like the 4% rule are conservative is because good financial planners know that taxes, fees, inflation and sequence of return risk are real things. And they’re the things that can blow up a retirement plan if you don’t make conservative estimates that properly account for them.

3) This is Not an Era of Fiscal Dominance.

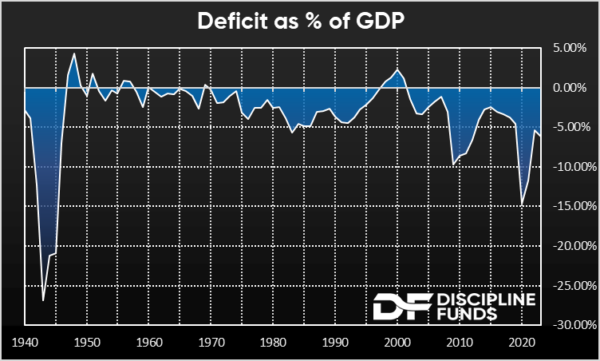

When inflation first surged in 2021 there were many compelling narratives about how we’re on the verge of a double bump in inflation. The two historical precedents for this were the 70s and 40s. The 1970s narrative didn’t last long because the oil price boom and wage price spiral never materialized. But the 1940’s narrative has been more compelling and persistent because the 40s were an era of “fiscal dominance”. And yes, we all know that the US government’s financial position has been, um, irresponsible in recent years. Fiscal dominance refers to an environment in which the government is printing so much money that it doesn’t even matter what the Central Bank does to counteract it because fiscal policy is so dominant.

The problem with this narrative is that this doesn’t look like an era of fiscal dominance. In fact, the current environment doesn’t look that much different than what we experienced in the 80s and 2010s where the budget deficit was consistently 4-6% of GDP. As of last month the budget deficit is 6% of GDP. That’s high by historical standards, but we’re coming off 15% and likely headed towards 4-5% so we’re getting fiscally tighter and the Fed’s policies are clearly having a strong impact. But more importantly, the 40s were a drastically different era because the deficit was over 15% for FIVE years. This wasn’t the one off sort of event that we saw recently. The 40s were a sustained effort to print money to fight WW2.

Of course, it’s probably fair to say that our fiscal position isn’t headed in the right direction. I don’t discount the potential that we could see an era of fiscal dominance in the future, but this ain’t it. So far, it appears that despite a relatively large budget deficit the Fed’s monetary policy tools have asserted a clear dominance in the fight against inflation.

1 – Ramsey does this by cherry picking a particular group of mutual funds that generated very high returns during the 1990s (before they became popular, of course). Those funds have not beat the S&P 500 since then, but he continues to promote them and their “high” returns. In addition to being a classic case of cherry picking past performance it ignores the fact that, in the last 20 years, these funds have generated closer to 5% after taxes, fees and inflation even when you include this period of outsized PAST performance.