Here are three things I think I am thinking about.

1) Work is for jerks. There was a viral rant going around Twitter all week from a young lady who hates her 9-5 job and commute.1 In a tearful video she explains how her 9-5 is sucking the life out of her and how she feels lost thinking that this is what adulting amounts to. She’s being dragged pretty relentlessly, but I feel her pain. Then again, I also have some unfortunate news for her – working from home won’t necessarily fix this.

I’ve worked independently or from home for 20 years now. I’ve always cherished my freedom and work/life balance, but it hasn’t always been that balanced. You see, the problem with working for yourself and being at home a lot is that you are uniquely dependent on yourself for motivation, discipline and efficiency. So there’s a big trade off here. Not only will you very likely make less money working from home, but you’ll also just generally be less efficient because your environment will leave you open to a lot more distractions and fewer opportunities to collaborate, network and grow.

But I have even more bad news for this young lady. It’s going to get a lot worse. Well, not worse, but definitely different and more challenging. What I mean by that is that one day you’re going to wake up with a husband and a bunch of kids and you’ll realize that life isn’t about you. It’s about all those other people. And you’ll feel a deep responsibility and a duty to provide for them. At least that’s what happened to me. But it’s all good. Work is an opportunity for me to provide something not only for the people I work for, but also for the family I am providing for. This isn’t really bad news. I’m actually having more fun than ever starting new companies, working on a new book, competing and just generally trying to juggle all the challenges of work and life.

So yeah, your 20s are tough because you are mostly a grunt working for other people on their time. But it’s also the best time because you have the energy to do things you won’t when you’re 40. And then when you’re 40 you’ll embrace your work, make a lot more money and your responsibilities will change. Life will always throw challenges at you. You can either look at the challenges as opportunities to overcome or dead ends that leave you in a doom loop. Either way, being young is when you pay your dues. And then when you get older you’ll proudly pay more dues knowing that the dues you’re paying are creating better opportunities for other people.

2) Is the Fed fumbling in the Red Zone? My economic outlook over the last few years can be summarized as follows:

- Covid created a bust that the government washed away with fiscal stimulus.

- The subsequent boom became highly irrational and created excess inflation which the Fed has been aggressively fighting.

- The economy has slowed materially and markets have corrected substantially as we digest the excesses of the boom.

- Aggressive Fed tightening creates the outlier risk of a credit event as inflation slows and potentially slows more than the Fed wants during a softening economic environment.

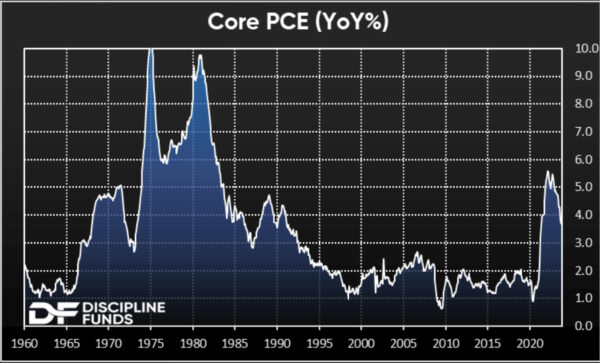

This morning’s core PCE inflation figure came in at 3.7% which was the slowest pace in many years. Yes, still too high, but the trend is solidly in the right direction and with all the downward pressure in commodities and housing there’s a strong probability that this trend will continue in the years ahead. So, we have low unemployment, just printed 5% GDP and the Fed is letting long interest rates continue to grind higher to the point where housing is likely to get even weaker. Despite this, it looks like we really do have a soft landing on our hands. Yes, it looks like they almost pulled it off. But to put the plane down without damage the Fed is going to have to ease rates back to a more sustainable equilibrium.

But the question now is whether they’ll be forced to put the plane down because of an emergency or whether they‘ll ease the plane down on their own volition. They’re in the perfect position to ease back. If I were Fed chief I’d be communicating an end to hikes and a halt in the balance sheet run off. This would send a strong signal to the bond market that it’s time to stop letting rates climb. But it also wouldn’t send the wrong message where people think easing is imminent. But instead of this they’re letting credit markets grind higher and banks weaken more. It all makes me wonder if they’re on the verge of fumbling the ball right when it looks like they might be on the verge of scoring.

3) Credit is Faltering. The primary transmission mechanism of monetary policy is through credit markets. Higher interest rates make it more expensive to borrow which increases the demand for money and reduces the demand for credit. This is one of the main reasons why the rate of inflation has been moderating in the last 18 months. If credit were easy the housing market would be booming, borrowing would be booming and aggregate demand would be much higher than it is.

Instead, credit is faltering. This is best reflected in rising credit spreads and the collapsing regional bank index which was down another 10% this week and is 20% off its recent highs. At the broader loan level, the rate of change in new borrowing has slowed to just 3.6%, which is the slowest rate of change since 2017. I wouldn’t say it’s at a point where you need to panic, but this is one of those signals where I look at the Fed and wonder how much they think about risk management. At this juncture the key question is which of these outcomes is worse:

- Inflation remains modestly too high and moderates to 2% over the coming few years.

- Inflation falls very fast because of a credit event.

The prior is uncomfortable, but hardly a horrific outcome. The latter, however, would likely coincide with a big surge in unemployment and a traumatic economic environment. And while the latter is less likely it’s a scenario that the Fed has to start taking seriously given their history of staying too tight for too long.

Strange times. Maybe the strangest of my career. But I guess that’s appropriate given that it’s Halloween weekend. Let’s all hope the Fed has this right and that the scary season ends this weekend.

1 – You know you’re old when people start calling you “sir”. You know you’re really old when you have to consciously refer to a recent female college graduate as “young lady”.