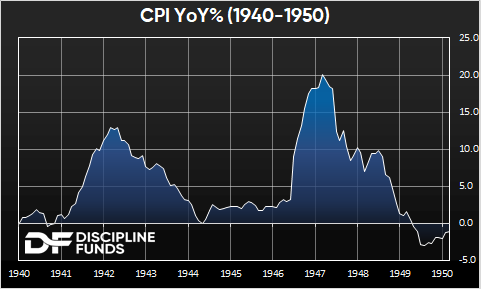

The Federal Reserve has expressed concerns about a double bump in inflation. That is a scenario where inflation surges and then jumps higher again for various reasons (such as the Fed letting off the brakes too early). The most common period of concern is the 1970s where inflation surged in the 1973-1975 period, cooled a bit and then surged higher from 1978-1980. We’ve argued that the 1970s are a bad proxy for this period and that’s been largely right so far. But another period that is commonly cited is the double bump inflation of the 1940s. But how similar is this environment to the 1940s? We don’t think it’s very similar for several reasons.

The 1940’s were a period of widespread economic turmoil and large secular macroeconomic trends including:

- Population boom following WW2.

- Broad global dependence on oil as an energy source.

- Supply chain hiccups during the war.

This was a perfect recipe for high inflation as the war disrupted supply chains, the global economy had non-diversified energy sources and populations boomed around the globe. When the global economy started to rebuild in 1946 you had a perfect confluence of events resulting in a sustained supply/demand imbalance.

In the 1940s the US population grew a whopping 15%. The current 10 year trailing growth rate is just half of that. The CBO forecasts population growth of just 0.3% per year for the next 30 years. Additionally, the population distribution by age is vastly different as the global economy gets older.

On the energy front the global economy was non-diversified compared to today and the boom in the automobile industry following the war resulted in a huge supply/demand imbalance. The price of oil rose 100% in 1946 which was the primary cause of the double bump in inflation.

The war created the perfect environment for a high inflation and the end of the war coincided with a unique population boom, industrial boom and supply chain issues that resulted in an unusual double bump in inflation.

Today’s economy is very different from the 1940s environment. Populations are growing meagerly, the supply chain issues from Covid are largely resolved, our energy sources are vastly more diverse and there is no post-war industrial boom to be seen. So, like the 1970s, we don’t see the 1940s as a good proxy for understanding the current risks to inflation.