If you looked at a chart of the yield curve (YC) in the USA you’d be absolutely convinced that this indicator is a recession predictor. After all, it has a nearly flawless track record predicting recessions in the USA. But if you looked outside the USA the data is much more mixed. This 2010 NBER paper found that the yield curve is not as predictive as you might think if you only looked at US data.

The story is nuanced in my view. Let me explain.

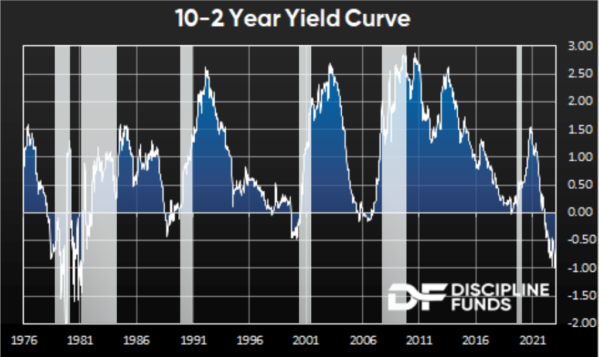

What is the Yield Curve?

The yield curve is the difference between the current 10 year T-Note yield and the 2 Year T-Note yield. When the curve is inverted it means the 2 year rate is currently higher than the 10 year rate. This is unusual because the yield curve usually slopes upward as investors expect to earn a higher yield for taking more risk across longer time periods. But the curve typically inverts when there’s a problem in the economy and the Fed views current inflation as being too high. So they raise the short rate to try to reduce inflation and this oftentimes gets reflected in the YC as an inversion. Many times, the Fed leaves rates too high for too long and growth slows much more than expected.

In and of itself the YC is not a recession predictor. It is a prediction about the future path of Fed policy (and inflation).

The Fed Funds Rate is the rate the Fed sets on overnight money to establish the demand for money necessary to get inflation to its 2% target. So, if inflation has been averaging 5% per year the Fed might set the FFR at 5.5% to increase the demand for money and bring inflation down.

Like a dog on a leash, the Fed controls the short end of the leash with absolute power as the reserve monopolist. The 2 year floats a little and the 10 year floats even more. The Fed lets the dog wander a bit and actually benefits from getting signals from the dog. The 2 year yield reflects the expected future average of 2 years of Fed policy. So, the current 4.75% 2 year yield is predicting that the Fed Funds Rate will average 4.75% over 2 years. The 10 year T-Note yield of 3.85% is predicting a 10 year average FFR of 3.85%. This is an implied inflation prediction since the Fed will only reduce the FFR if inflation is lower over the next 10 years than the current overnight positioning implies.

What Does the Inverted Yield Curve Predict?

So, an inverted yield curve is not really predicting recession. It’s predicting that the Fed will reduce rates in the future because inflation is likely to be lower than it presently is. Another way of thinking about this is current growth is too hot and the Fed has to set a very tight overnight rate to get the economy to slow. This shows up in the yield curve as a prediction that the Fed will win its battle and lower inflation (and lower growth) is likely to occur over the course of the next 10 years. But as the global evidence shows this doesn’t necessarily mean a recession is on the horizon.

This is important because we often see these discussions about how the “bond market is smarter than the stock market”. I don’t think this is quite right. When the yield curve is inverted the bond market is predicting lower future growth and lower future inflation. They’re not predicting recession, per se. And in fact, lower inflation might end up being very good for stocks and the economy (assuming the Central Bank doesn’t stay tight for too long). At the same time, a decelerating economy with an overly tight Fed is a recipe for rising recession risk. We’ve seen this across a slew of data in the last 12 months.

As we recently noted, you don’t want to think of the economy and the markets as an on/off switch. If you look at an indicator like the YC that’s inverted you might conclude that you need to flip the switch off on your stock positions. This sort of binary thinking is more like gambling than anything else, but great investors don’t think in binary terms. They think in probabilistic terms. And one thing we know from inverted yield curves is that they tend to occur around periods of rising economic and market risk. This means it might make sense to reduce stock market risk, but it isn’t a siren that tells you you need to jump into your bunker.

In sum, it’s best to think of the inverted yield curve as a Fed Funds Rate prediction, which is an implied prediction of future relative inflation. This often correlates with rising recession risk and rising market risk, but in and of itself the yield curve is not a recession predictor.