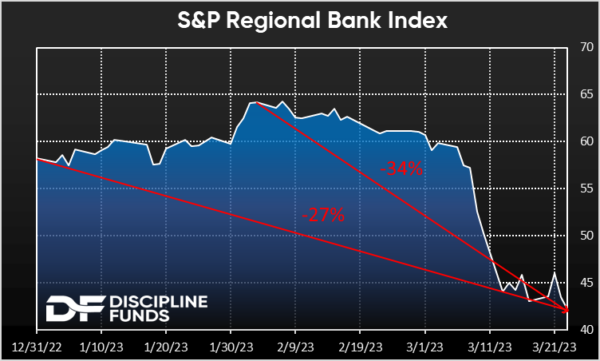

This week’s chart of the week shows the S&P Regional Bank index performance year-to-date. The Index is down -27% this year and -34% from its high. Pretty big numbers.

Banks are obviously getting a lot of the attention this year given the recent developments with SVB and some other regional banks. But are the banks actually causing the fire or are they merely a symptom of the fire?

When I talk about the monetary system I always like to start with first principles and operational realities. I like to think of the financial system like a car with a bi-polar driver. That is, there are certain operational facts about how the car drives, but the thing that makes predictions about this vehicle difficult is that the driver does crazy and unpredictable stuff at times. It’s why economics is as much social science as hard science. Understanding operational realities is important because you need a baseline understanding for how the car works so you can understand the parameters within which it can operate. For instance, when people scream about silly things like hyperinflation you can often fall back on operational realities knowing that the car operates in a specific way and even if the driver is insane they can’t make the car fly into space.

If you missed my latest Three Minute Macro video I highly recommend it because we touch on this specific topic – hyperinflation and the operational realities of Fed lending as it pertains to the banking system. Some rather famous people were screaming about hyperinflation in response to the bank rescue and there is virtually no operational way the new Fed program can actually cause that to happen. In other words, if you understand how the car operates you can calmly ignore these sorts of hyper-emotional narratives.

In the context of the recent bank panic it’s important to understand how unusual the recent runs were. After all, these weren’t garbage loans gone bad. SVB held mostly high quality government bonds and their loan book was largely intact. This wasn’t a 2008 style bank panic where the banks were insolvent because their customers were defaulting on bad loans. This was mainly just a case of mark-to-market losses and a flighty non-diversified depositor base. But that doesn’t mean it wasn’t real.

I like to think of banks as the plumbing in our financial house. When the pipes burst it’s usually the result of something else. For instance, in this case it was actually the boom/bust of COVID and the way SVB’s clients were bleeding money which bled SVB of deposits. Add in the inflation that resulted from the COVID boom and you layered in the Fed rate hikes which ultimately rendered SVB insolvent on a mark-to-market basis. But the key point is that the flooding in these pipes was the result of something else and in this case it was the private equity market going up in flames and an arsonist (the Fed) who tried to put that fire out by pouring gasoline on it. So yeah, the banks caught on fire, but the fire didn’t originate in the pipes.

The key point in all of this is that the banks are a distraction to what is really going on here. And what’s really going on is that there was a raging fire in the economy during the COVID boom and the damage from that fire is now becoming apparent during the bust. Private equity is one of the first places where it’s appearing. But there are other problems out there including the downturn in residential real estate and commercial real estate. And I don’t think the fire is done causing damage even if our arsonist might have already put on his plumber’s hat and fixed the bank piping.