If you missed the early weekend reading then please see here. But if you really want to ruin your weekend then please keep reading this special labor market edition of weekend reading.

How about that labor report? The October employment report came in at just 12K. It was a very messy report given the impact of the prior month’s hurricane and the big Boeing strike. Some estimate that these factors took about 80K jobs out of the report. It’s impossible to know what the exact figure is, but the stuff I focus on showed more of the same slowing trends. Specifically:

- The quits rate in the JOLTS report show significant softening. People quit when the labor market is strong so a soft quit rate is consistent with softening labor conditions.

- Long-term unemployment jumped to 1.7%. This is the surest sign of a softening labor market as people who are looking for work remain unemployed for longer and longer.

- Temporary help fell significantly. Temp help tends to lead broader employment since firms hire and fire temporary workers before firing or hiring full time workers.

There’s no need to panic over all of this. My recession rule is at 33% and rising, but it needs to be over 50% to trigger a recession warning. We’re not close to that yet and haven’t been for the entirety of the last few years even while many other recession indicators triggered a warning. So the Fed doesn’t need to be moving too fast with cuts. At the same time there is still considerable concern over the future of inflation and many analysts are still concerned about another big surge in inflation. I still don’t see it.

Here’s how I would think about this environment and the current state of affairs relative to where we’ve come from:

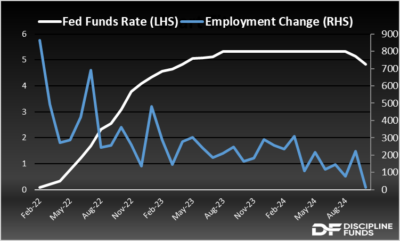

- Nominal GDP was averaging 6.6% in 2023 and employment was averaging 244K jobs per month. That’s an environment where demand is still very strong and likely to contribute to rising prices. A 5% Fed Funds Rate is totally appropriate in that environment and we now know, for a fact, that the FFR helped push inflation down.

- Nominal GDP came in at 4.9% last quarter and is trending down. The latest RGDP estimate is just 2.3% (which implies NGDP of about 4.5%). Employment has averaged 195K per month so far in 2024, but has trailed off to just 145K over the last 6 months even if we ignore the latest report.

- Recent headline PCE was just 2.09%, .09% above the Fed’s target rate. Some wage readings have been a tad worrisome, but broader inflation indicators like commodity prices still show no signs of a big inflation surge.

So, the Fed can see the landing zone and they’ve appropriately started their descent. You don’t wait until you’re at the landing zone to start landing. You start well before you reach your target. So there’s nothing wrong with initiating the descent when we’re still above target. And given the slowdown in NGDP and employment I see no problem with a modest pace of cuts in 2025. They might move slower than expected, but I don’t see how a 5% Fed Funds Rate is appropriate in an environment with all these slowing trends.

In short, the important risk analysis has to consider whether a surge in inflation looks more likely than a surge in recession risk and unemployment? I suspect you know my answer, but the chart at the right makes that pretty definitively clear in my opinion.

Have a great weekend.