Here are some things I think I am thinking about.

1) Tariff counterfactuals.

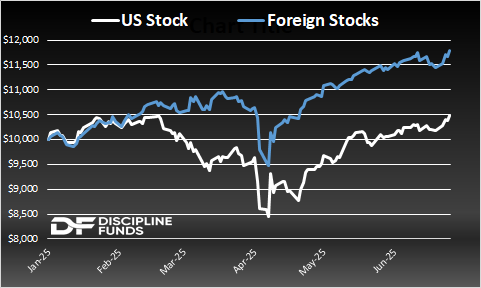

The stock market has returned to where it was before the whole tariff fiasco happened. And now I am seeing people say “see, the tariff worries were all overblown!” The endgame here played out more or less the way I said it would back when I pegged 70% odds of “scenario 2” in my April 19th note. Trump mostly caved on China and the effective tariff rate has now dropped to a rate that is still high, but nothing remotely close to the embargo style levels we had in mid-April. And the markets have rightly bounced back. But that doesn’t mean there was no damage done.

When we assess the impact here we have to look at it in relative trade terms. For instance, the US Dollar has fallen 6.5% since the beginning of the year when more and more protectionist measures were implemented. Some people might say a falling Dollar is a good thing, but I don’t see it that way. You would never look at a collapsing currency in a place like Argentina and say “oh look, they’re more competitive now!” They technically are, but their currency collapsed because they have hyperinflation and their economy is less competitive on a relative basis. Likewise, it’s been a good thing that the USD was rising for so long because it’s a coincident indicator that the USA is doing better in relative terms. We want our currency to rise because it’s a symbol that there’s strong demand for our currency and that we’re doing better on relative terms.

This is most evident in relative stock prices this year. While the US stock market is back to where it was before the whole tariff thing started, foreign stocks are now up 19% year to date. This is a sign that the markets expect the rest of the world to become more competitive in relative terms. Which is exactly what you’d expect from a policy like tariffs, which hurt our ability to compete on the global stage. This doesn’t mean we’re doing badly. It means we’re not doing as well as we otherwise would be. Which is exactly why economists call tariffs the “invisible tax”. Your economy might do just fine in absolute terms, but you don’t see that you’re doing worse in relative terms in large part because you don’t see the counterfactual outcome. It’s very likely that, if we hadn’t done any of this tariff stuff that the USA would be the blue line on that chart.

Anyhow, it’s a good thing that this isn’t causing widespread absolute damage to the US economy. But that doesn’t mean it isn’t causing relative damage to the US economy.

2) Book revisions.

Speaking of revisionist history – I handed in the very final manuscript for my second book last night. Well, technically this is my third book since I wrote the world famous thriller “Sleep Bear’s Sleepy Time” for my daughters. The final title of the book is:

Your Perfect Portfolio – the ultimate guide to using the world’s most powerful investment strategies.

This one’s really fun. I tore apart 20 of the most famous investment strategies and even discussed a few of mine (including a totally original one that I think is awesome). Some are very basic, others are complex, but they’re all powerful in their own unique way. I also wrote entirely separate sections on essential concepts to understand and some fun loose ends. I feel like I dumped everything I know about investing into 260 pages. And I tried to do it in a more conversational way than I did with Pragmatic Capitalism, which was pretty dense at times. I think you guys are really going to like this one and more importantly, I think you’re going to find it educational, useful and ACTIONABLE as I tell you how to implement every single portfolio.

We are scheduled to publish on January 6th of 2026, but it should be available for pre-order before that. I’ll let you know as we progress.

3) Why isn’t the Fed cutting rates?

JD Vance asked a good question on Twitter:

“I’d love to hear an argument for why Powell cut rates 50 points right before an election but can’t do it now with inflation lower.”

Trump is very eager to cut rates to stimulate growth. And I don’t disagree with him. I think inflation has come back essentially to target and that the labor market is showing enough fragility that you could easily get rates down to 3.5% or so and feel okay about how loose policy is. And let’s not forget that housing, despite prices being somewhat robust, has been in the doldrums for years now. Most importantly, with inflation at 2.1% on headline PCE and 2.5% on core, I think the Fed can pretty much declare victory. Sure, it’s not exactly at their 2% target, but it’s below the historical average and close enough to target.

But this isn’t the slam dunk argument that it was a year ago when they cut 50. When the Fed cut 0.5% last September the inflation rate was also 2.1%, but the rate of inflation had been on a one way trend from 7.2% down to 2.1%. There had been almost no signs of a change in the downward trend and so it was pretty clear that a 5%+ rate was too restrictive relative to 2.1% inflation. And so they cut 1% over the course of the next few quarters and now the Fed Funds Rate is 4.1%. But the problem now is that inflation expectations and inflation itself have been mostly sideways for the last few quarters. And it had been trending from 2.1% to 2.6% over the 5 month period since September. So the worry was that their cutting was sparking a little inflation. And then of course we got the big tariff scare. And although the Fed said it wasn’t likely to cause sustained inflation I can see why they would sit on their hands just to be sure. After all, 4.1% is restrictive, but it’s not nearly as restrictive as 5.1%.

The bottom line is, I am not especially worried about inflation at present. And I generally agree with the White House that the Fed should be cutting further. But I can also understand the Fed’s position that it’s okay to wait and see. After all, it’s not like the economy is cratering or anything. There’s no need to be overly zealous in either direction. So I can see both sides of the argument here even though I lean towards a moderate pace of further cuts.

Well, that’s all I got for now. I’ve written about a billion words in the last few months and I am tired so excuse me if I stop here. I’ll be in better form shortly. Until then, thanks for reading and stay disciplined.