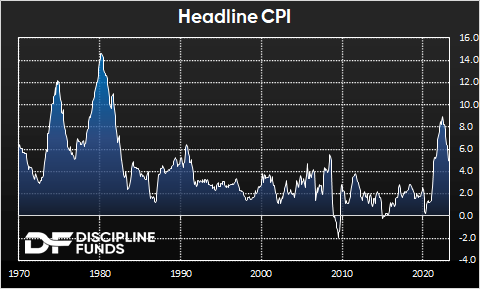

One of our big themes for this year was that it would be the “year of disinflation”. That is, a falling rate of positive inflation. And so far that appears to be dead on. The latest headline CPI came in at 4.9% which is well off the 2022 high of 8.9%.

Despite this the Core CPI (minus food and energy) is still far too high at 5.5%. While inflation is trending in the right direction it’s still well above the Fed’s target rate of 2%. And we don’t think it’s going to get there any time soon. But we do think it’s going to get there. It’s only a matter of time.

The really good news in this latest inflation report is that shelter remains a large contributing upside factor. The reason this is a good thing is because shelter is 35% of CPI so it can drive big trend changes in the CPI. It’s been one of the primary factors driving inflation higher and we’re now cresting that peak.

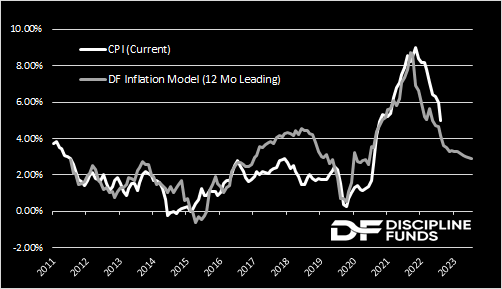

The reason shelter lags so much is due to the way the BLS surveys consumers. What they do is try to reflect the manner in which shelter contracts reflect “sticky” prices so rents are updated every 6 months. For instance, your rent doesn’t change every month. It typically changes once a year and so inflation can be rising, but you won’t experience that increase until the landlord updates your contract. So there’s a temporal lag in the way consumers actually experience shelter inflation whereas CPI is reported in a real-time manner. This is good news for inflation going forward because shelter inflation in the CPI is near its cyclical highs of 8.1% whereas real-time rent data shows that there’s been disinflation in rents for over 6 months. This means that the shelter component of CPI is likely to put downward pressure on overall CPI in the coming years. And yes, this is going to take years now. So the biggest component of CPI is about to become a large contributing disinflationary factor in overall inflation.

All that said, shelter inflation is still running at 6% using real-time metrics such as the Zillow Rent Index (down from 17% last year) so while it’s becoming a large disinflationary force inflation is unlikely to reach the 2% target any time soon. Our current estimate for year-end core PCE (the Fed’s preferred measure) is 3.5%. We expect CPI to trend towards 3% as the year goes on. But all that leaves the Fed in a precarious position where they have to defer towards the risk being to the upside (for now).

All this combined means that there’s no pivot coming. The Fed remains highly concerned about a snapback in inflation similar to what we saw in the 1970s. So they’re likely to remain very restrictive and keep rates above 5% until they can be certain that inflation is dead, dead, dead. We’re not there yet, but we’re moving in the right direction.